Why the Best Time to Stay Invested Often Feels Like the Worst

The first quarter of 2026 has created a lot of uncertainty. There are plenty of reasons why you might feel unsettled.

Geopolitical tensions in the Middle East have pushed oil prices higher and added to concerns about inflation, while central banks, including the Reserve Bank of Australia, remain alert to the risk that temporary price shocks become persistent.

When markets turn volatile, the instinct to “do something” can feel overwhelming. That is entirely human. It is also where many investors come unstuck.

Headlines do not automatically justify changes to a well-constructed long-term financial strategy.

The economy and the sharemarket are not the same thing. Markets are forward-looking and often begin recovering before the economic data does. Research from Dimensional Fund Advisors notes that stock returns can be positive even during recessions because markets are constantly pricing expectations about what comes next, not simply what is happening now.

One of the biggest mistakes people make during periods of market stress is assuming that the safest move is to step aside, move to cash, and wait for things to settle down. In practice, the best days often arrive right in the middle of the worst ones.

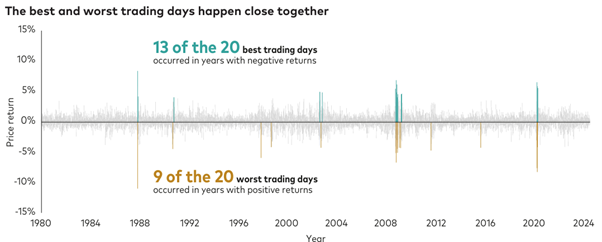

Vanguard recently published analysis[i] of global sharemarkets showing just how closely good and bad days cluster together. Looking at the 20 best and 20 worst trading days since 1980, Vanguard found that 13 of the 20 best trading days occurred in years when markets delivered negative returns, while 9 of the 20 worst trading days occurred in years with positive returns. In other words, strong recovery days do not wait until investors are feeling calm again. They tend to show up when uncertainty is still high and confidence is still low.

Data shows the MSCI All Countries World Price Index

J.P. Morgan’s data[ii] makes the point even more sharply. Over the past 20 years, 7 of the market’s 10 best days occurred within 15 days of one of the 10 worst days. It also found that an investor who stayed invested throughout that period earned an annualised return of 10.6%, while an investor who missed just the 10 best days earned only 6.4% annualised. That is a very large gap (especially when you factor in the compound returns), created not by poor stock selection, but by poor discipline.

This is why trying to time the market is so difficult. To succeed, you do not just need to know when to get out. You also need to know precisely when to get back in. And unfortunately, the re-entry point often comes when the economic news still looks awful, sentiment is still weak, and most people are still convinced there is more pain to come. Markets are forward-looking creatures.

Vanguard also looked at what happens when investors switch to cash after weak market periods. The findings are not encouraging for would-be market timers. An investor who moved to cash for 3 months after a weak patch had a 63% chance of underperforming a balanced 60/40 portfolio, with median underperformance of 1.9%. Stay in cash for 6 months and the probability of underperformance rose to 74%, with median underperformance of 5.8%. Stretch that to 12 months, and the probability rose again to 80%, with median underperformance of 10.8%.

That is the real cost of panic-selling. It is not just that you crystallise losses. It is that you often miss the part that does the heavy lifting when returns recover.

For long-term investors, the lesson is not that markets are easy. They are not. Volatility is uncomfortable, headlines are noisy, and downturns can feel personal when your portfolio balance drops. The lesson is that a sound investment strategy should be built with this reality in mind. Your advisers at Lorica Partners expect, and plan for, market volatility.

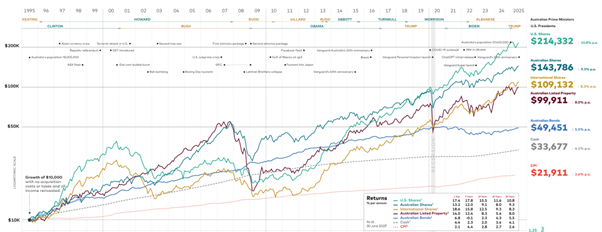

The long-term data is a useful antidote to short-term anxiety. Vanguard Australia’s 2025 Index Chart shows that $10,000 invested in Australian shares on 1 July 1995 would have grown to $143,786 by 30 June 2025, compared with $33,677 in cash. US stocks did even better, growing to $214,332. That period included the tech wreck, the global financial crisis, COVID, wars, inflation shocks and a long list of reasons people thought “this time is different.” Usually, it wasn’t.

When markets fall, it is natural to want certainty. But certainty is rarely on offer. Discipline is.

And in investing, discipline has a much better long-term track record.

Current events reinforce the importance of focusing on the things you can control - your cash buffer, your spending, your debt structure, your diversification, your costs, and whether your portfolio is still aligned to your long-term objectives. Those are useful decisions. Trying to jump in and out of markets because the world feels uncertain usually is not.

Author: Rick Walker

[i] Discipline may be the best defence in a downturn – Vanguard 2026

[ii] https://privatebank.jpmorgan.com/nam/en/insights/wealth-planning/the-power-of-intent