Research-Backed Investment Strategies

At Lorica Partners, our investment philosophy is grounded in decades of academic research which revolutionised the way we think about investing and portfolio construction. In this article, we pay tribute to the academics instrumental to developing these foundational theories, explore the impacts of their research and explain how we put the theories into practice.

in theory…

Modern Portfolio Theory

Harry Markowitz (1927-2023) was a Nobel Prize winning economist celebrated for conceptualising “Modern Portfolio Theory” in 1952.

Prior to his theory, the typical investor approach was to analyse individual assets by looking at the risk specific to that asset – for example, by preferencing government bonds over higher risk corporate bonds, or blue-chip stocks over much smaller companies. In other words, most investors constructed their portfolio by selecting a number of individual ‘safe’ assets.

But Markowitz saw a significant flaw in this approach – although each asset assessed separately might have lower-risk, the covariance and correlation between assets in a portfolio could result in overall returns which were highly volatile and subject to big swings. Instead, Markowitz identified that diversification could benefit a portfolio by ensuring each asset doesn’t move exactly in line with each other asset, ensuring the volatility of the overall portfolio is reduced to result in more consistent and stable returns.

By spreading investments across a variety of assets with different risk and return characteristics, investors could achieve a more stable overall portfolio performance.

More stable returns always equate to higher portfolio values, as this simple example shows:

Each portfolio has an average annual return of 8%, but Portfolio 1, which has the smoothest annual returns, produces the highest end portfolio value of $146.93.

The concept that adding a seemingly risky asset to a portfolio could actually reduce the portfolio's overall risk is a key takeaway from Modern Portfolio Theory. This happens when the asset's price movements are not perfectly correlated with the other assets in the portfolio, effectively diversifying the risk.

The following chart shows how increasing the number of assets in a portfolio reduces the risk (measured by standard deviation of returns) of the portfolio. Of course, risk cannot be eliminated by diversification, so market risk always remains.

Capital Asset Pricing Model

Just over a decade later in the early 1960s, William Sharpe (1934-present) developed his own Nobel Prize winning theory - the Capital Asset Pricing Model (CAPM), building on the foundations of Modern Portfolio Theory. CAPM calculates the expected return of a particular asset by assuming the return is composed of:

Risk-Free Rate represents the baseline return an investor can expect to earn without taking on any investment risk. It's usually associated with government bonds, particularly those with a very low default risk, such as AAA-rated bonds.

Market Risk Premium is the additional return an investor demands for taking on the risk of investing in the stock market instead of the risk-free asset.

Asset-Specific Risk Premium takes into account the asset's sensitivity to market risk. It's often measured by beta, which quantifies how an asset's returns move relative to the overall market's returns. Higher beta assets are expected to have higher returns to compensate for their higher exposure to market risk.

CAPM’s elegance lies in its ability to provide a simple formula to calculate an asset’s expected return based on these three components. It helps investors assess whether an asset is providing an appropriate level of return given its level of risk.

Multi-Factor Models

Fast-forward another decade to the early 1970s, and Bob Merton (1944-present) (another Nobel Prize laureate) expanded on CAPM by developing the Intertemporal Capital Asset Pricing Model (ICAPM). ICAPM recognised the limitations of the simplistic CAPM framework and instead theorised that investors are concerned with a variety of additional future risks which can impact their long-term investment horizon. ICAPM opened the door to future research of multi-factorial models which seek to understand investment returns by reference to a variety of contributing variables.

The most influential of these multi-factor models emerged in 1993 developed by Nobel laureate Eugene Fama and Kenneth French. The Fama-French Three-Factor Model estimated/explained asset returns by reference to:

a market risk factor (like CAPM)

a size (market cap) factor (Size Premium), and

a value (book to market ratio) factor (Value Premium).

This model not only improved the understanding of asset pricing but also provided a framework for investors to account for more dimensions of risk and return in their decision-making. By considering size and value factors alongside market risk, investors gained a more comprehensive view of asset performance.

The model was expanded to five-factors in 2015 with the addition of:

a reinvestment factor, and

a profitability factor (Profitability Premium).

The addition of the profitability factor was largely recognisant of Professor Robert Novy-Marx’s research in 2013 which empirically linked gross-profitability as a long-term driver of expected returns.

in practice…

So, what impact have these theories had on investment philosophy generally, and Lorica Partners’ investment strategies in practice?

Modern Portfolio Theory was instrumental in demonstrating the value of diversification. By spreading investments across various markets, industries, and asset classes, investors can reduce their exposure to specific risks associated with individual securities or sectors. This approach is like having multiple "baskets" for your investments, which can help mitigate the impact of poor performance in one area.

Portfolio rebalancing is a natural consequence of Modern Portfolio Theory and CAPM theory – by rebalancing your portfolio whenever it deviates substantially from your target asset allocation, over time, you will sell more overvalued assets while buying more undervalued assets.

Having a solid understanding of these theories can help investors make more rational and informed choices rather than being swayed by market trends or emotional reactions. A robust investment strategy built on these theories encourages a disciplined approach, which is especially important during periods of market volatility.

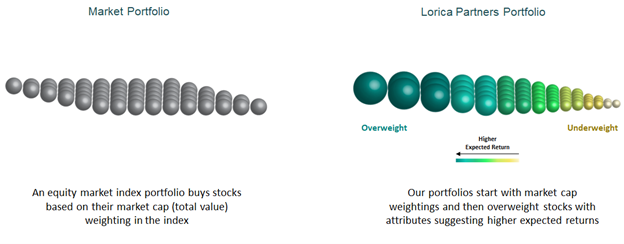

Lorica Partners’ equity portfolios are tilted away from the market to own more stocks with attributes expected to deliver the Size Premium, Value Premium and Profitability Premium, as this graphic shows:

By investing in a large pool of assets, investors are guaranteed to be holding at least some of the winners. The graphic below shows in 2023, only 20 of the top 500 stocks have driven most of the stockmarket return:

Source: Just 20 Stocks Have Driven S&P 500 Returns So Far in 2023 (visualcapitalist.com)

We have previously written articles explaining only a handful of stocks drive the overall market return which is why we do not advocate buying direct stocks: https://loricapartners.com.au/insights/2020/6/3/the-perils-of-owning-individual-stocks-more-losers-than-winners-jcsfh

Research has consistently shown that active fund managers have difficulty exceeding market returns. Instead, Lorica Partners implements investment strategies which incorporate the empirically time-tested research of these big-brain-names in the finance world. We achieve this by starting with a market portfolio, then looking to funds that have greater weighting in assets that have the proven characteristics from the multi-factor models of stronger returns in the long-term.

If you want more evidence, type “Research-Backed Investment Strategies” into Chat GPT!

Author: Rick Walker