Name Recognition is not an Investment Strategy

Walk down the cereal aisle and you’ll see it in 10 seconds.

One box is Special K with the “health halo” packaging. Next to it is the supermarket brand “toasted flakes” that tastes… suspiciously similar. Different label and a tidy premium for the comfort of a familiar logo. (In my brief career at Goodman Fielder I learned the ingredients between No Frills and branded items were often identical – the additional costs for the branded product were for the coloured packaging!)

Investing works the same way. A well-known fund name feels safer, even when the underlying ingredients are basically identical.

What the research is saying

A recent U.S study[i] tested something simple: show people two identical S&P 500 index funds (same holdings, same fees), then change only the label. One looked like it came from a well-known institution; the other had an unfamiliar name.

People allocated 65% of their money to the familiar label and assumed the unfamiliar option was riskier, even though it wasn’t.

The bigger (and slightly awkward) point: this bias doesn’t disappear once people get “sophisticated”. Even professional advisers show strong preferences for brand-name products and benchmarks.

US advisory firm IFA compared active funds from major fund families against their benchmarks. The results were remarkably consistent:

Goldman Sachs: 69% of 97 funds underperformed their benchmark or didn't survive. Just 1% achieved statistically significant outperformance.

Morgan Stanley: 88% of 163 funds underperformed.

Even Vanguard's actively managed funds follow the pattern. Despite the firm's reputation for low costs, 63% of its 87 active funds underperformed (yes, not all their funds are index trackers). Not even one produced statistically significant alpha (meaning outperformance of its benchmark).

The “star manager” story rarely ends well

It’s tempting to assume that a fund manager with a great 3–5 year run has “the knack”.

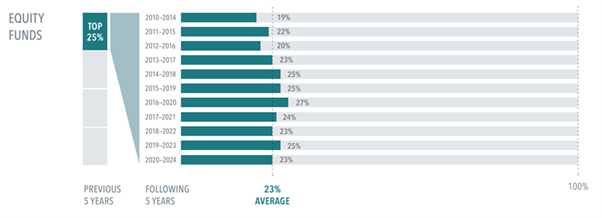

But persistence is the issue. For example, on average only 23% of U.S funds in the top quartile (25%) of previous 5-year returns maintained a top‐quartile ranking in the following 5 years.

Source: Mutual Fund Landscape, Dimensional Fund Advisors

A recent Standard & Poor’s report[ii] showed none of the top-quartile U.S domestic equity funds as of December 2020 remained in the top quartile over the following four years.

Why big names often disappoint

There are two very unromantic reasons:

1. Marketing is not free - The fund manager business model is built around gathering assets. A fund that grows from $1 billion to $10 billion generates ten times the fee revenue regardless of whether it beats its benchmark. Big brands spend money to become bigger brands. That cost doesn’t come out of the CEO’s pocket but from investor fees and fund economics.

2. Arithmetic is undefeated - Economist William Sharpe put it bluntly in 1991: before costs, active investors as a group are the market. After costs, they must underperform the market by roughly their costs. That’s not an opinion. It’s maths.

If the main reason you like an investment is “I’ve heard of them,” or “They’re everywhere,” that’s a cue to slow down. Brand comfort is a feeling, not a return driver.

The same applies to buying direct stocks. Buying a brand you are familiar with or jumping on the bandwagon is no guarantee of strong returns. As COVID started in March 2020, CSL was the market darling, with its share price around $314. Since then, the share price is down -49% whilst the Australian stockmarket is up +63% over the same period.

What to trust instead

A better filter is boring, but it works:

What do you actually own? (asset class exposure, diversification, risk)

What does it cost all-in? (management fees, admin, hidden frictions)

Is the process repeatable? (or is it “trust Dave, he’s a legend”)

Does the strategy stack up over decades?

The primary fund manager we use to access public markets is Dimensional Fund Advisors. Dimensional builds portfolios using academic research, and they’ve long worked with leading researchers (including Nobel Prize–winning economists, three of whom are currently on their Investment Committee) to rigorously test how their approach is designed and implemented.

Morningstar recently awarded Dimensional its 2025 “Exemplary Stewardship” recognition, placing it among a small group of global firms to receive the highest “Parent Pillar” rating. That wasn’t a trophy for bold performance claims but recognition for putting investors first.

None of that guarantees better returns. Nothing does. But the business model matters: if a firm needs advertising to grow, someone must pay for the billboards, and that “someone” is usually the investor via higher fees. A firm that wins trust through process and credibility doesn’t need the same marketing spend.

Almost none of our new clients have ever heard of Dimensional when we introduce them to their portfolio. With almost zero marketing spend, Dimensional now manages $1.4 trillion globally (that is $1,400 Billion), demonstrating we are not alone in supporting a scientific approach to investing.

Author: Rick Walker

[i] The Wharton Pension Research Council in November 2025

[ii] SPIVA Persistence Scorecard

Thanks to IFA for the inspiration for this article - https://www.ifa.com/articles/psychology_label_familiar_names_make_poor_investments