Financial Market Update - 30 June 2026

Strong returns, shifting leadership and no shortage of uncertainty

The first half of 2026 gave investors another reminder that financial markets rarely wait for uncertainty to disappear.

Markets absorbed war in the Middle East, disrupted energy supplies, renewed inflation concerns, higher interest rates and continuing uncertainty over trade policy. Yet global shares generally advanced, supported by resilient company earnings and extraordinary investment in artificial intelligence. (Asset class returns are shown at the end of the article).

The path was anything but smooth. It seldom is.

Artificial intelligence remained the dominant market theme

AI continued to influence both economic activity and sharemarket returns.

The first stage of the AI boom was dominated by a small number of large US technology companies. During the June 2026 quarter, leadership increasingly shifted towards the businesses supplying the infrastructure required to make AI work, including semiconductors, memory chips, servers, data centres and electricity.

The scale of investment is remarkable. Macquarie estimates that listed US technology companies intend to invest around US$580 billion during 2026, with a further US$900 billion planned across 2027 and 2028. This investment is becoming a meaningful contributor to economic growth and corporate earnings.

US technology company earnings were also particularly strong, growing by around +32% compared with the previous year. However, several established software and internet businesses weakened (e.g., Salesforce, Adobe) as investors questioned whether AI would enhance their businesses or ultimately disrupt them.

Markets do not yet know the answer. Neither does anyone else, despite the confidence with which some forecasts are delivered.

Our expectation is that AI will be less like a single new industry and more like electricity or the internet: a technology that spreads throughout almost every industry. Existing businesses will use it to improve productivity, reduce costs and develop better products. Some companies will adapt successfully. Others will not.

The economic benefits could be substantial, but that does not mean every AI-related investment will be successful – just like the 1990s when the internet arrived.

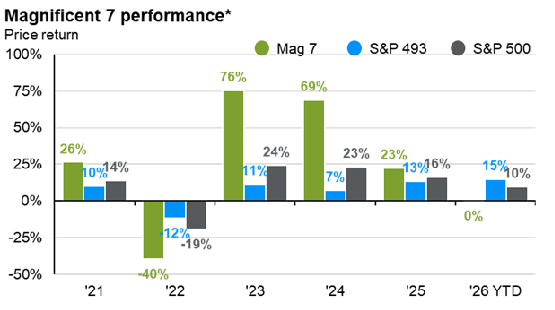

Market leadership broadened

Although AI remained central to markets, returns became less concentrated during the quarter.

Emerging markets were among the strongest performers over the first half of the year, helped by their exposure to semiconductor manufacturing and technology hardware. Europe and Japan also performed relatively well, while Australia lagged markets that have greater exposure to the AI infrastructure boom.

Within the US market, the Magnificent Seven stocks had a mixed 12 months. Whilst Alphabet’s (Google) stock price doubled, Meta (Facebook) and Microsoft were both down over -20%.

Source: JP Morgan

Markets are generally more resilient when returns are being generated by a broader range of companies, countries and industries rather than depending on a handful of very large businesses. And there were also reminders to investors of the risks of owning direct stocks over the past 12 months.

In Australia, several “blue chip” stocks experienced significant one days falls in the past year, including Cochlear (down -39.4% on 22 April 2026), Woolworths (down -16% on 19 August 2025) and CSL (down -17% on 18 August 2025). In fact, since February 2020 when CSL became the largest stock on the ASX, its share price is down -61% whilst the overall Australian stockmarket is up +21%.

Oil prices rose sharply—and then fell almost as quickly

The conflict involving the United States and Iran created the most significant geopolitical risk over the past year.

Disruption to traffic through the Strait of Hormuz initially pushed oil prices sharply higher. That raised concerns about inflation, household spending and the prospect of further interest-rate increases.

By the end of June, however, renewed shipping traffic and an initial agreement between the US and Iran had helped bring oil prices back close to where they had been before the conflict began. This retreat reduced the immediate risk of a severe global energy shock.

The risks have not disappeared. Reopening a shipping route on paper is different from persuading insurers, shipping companies and energy producers that it is safe to use. Oil prices are therefore likely to remain volatile.

Interest rates remained a source of pressure

The fall in oil prices provided some relief, but inflation remained above central-bank targets.

In the US, stronger economic and employment data reduced expectations of near-term interest-rate cuts. Bond markets reacted by pushing short-term yields higher, although longer-term yields were more stable.

The situation in Australia remained more difficult.

Australian households entered the year carrying high levels of debt and were then required to absorb three further interest-rate increases. Westpac expects underlying inflation to remain around 4% through the remainder of 2026, while the Reserve Bank’s forecasts do not show inflation returning to the middle of its target range until around mid-2028.

Falling oil prices may prevent further immediate pressure, but domestic inflation remains persistent.

The Reserve Bank therefore faces an uncomfortable choice. Rates high enough to restrain inflation also weaken household spending, housing activity and business confidence. Rates that are reduced too early risk allowing inflation to become more entrenched.

Australia’s deeper economic challenge

Australia’s economic weakness is not simply a cyclical story about interest rates.

For many years, strong population growth lifted overall economic activity while masking weak productivity growth and limited improvement in living standards. Investment in housing, infrastructure, energy and productive capacity did not keep pace with demand.

Households are reducing discretionary spending as higher mortgage repayments and essential living costs absorb more of their income. Business investment has improved, but much of that strength has been concentrated in data centres and digital infrastructure. These investments should eventually support productivity, although a significant proportion of the equipment is imported, limiting the immediate benefit to domestic activity.

Sydney Property Prices

The media has widely documented the softening of Sydney property prices since 2025, however numerous estate agents spoken to by the Lorica team in recent weeks indicate actual property prices are currently below what is being reported, as the data used is generally 3 months old. Some of the comments we have heard include:

The latest tax changes have had a significant impact across the market; we have not seen an investor since the Federal Budget announcements.

When rates were at their lowest someone who could borrow $3 million can today borrow $1.8m. That is a massive impact upon purchasing power.

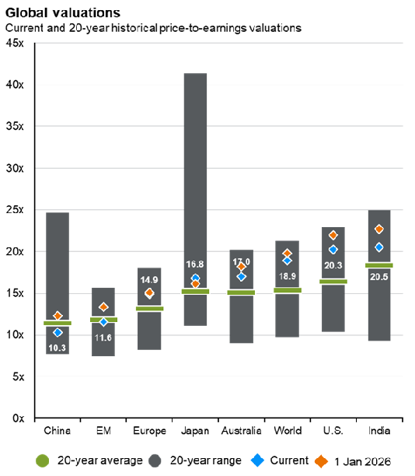

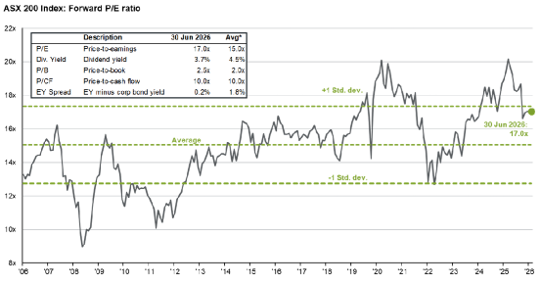

Stockmarket valuations

Current market valuations remain above long-term averages in most markets:

Source: JP Morgan

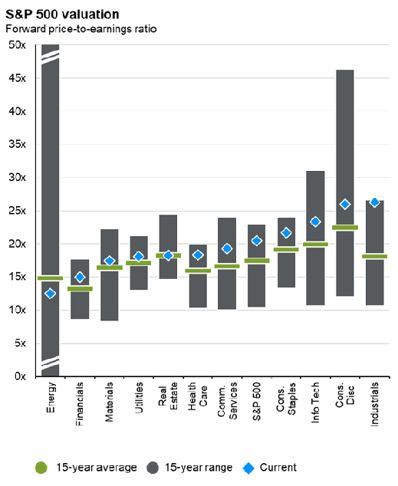

In the US, consumer discretionary and industrials are now trading on multiples higher than information technology, reflecting the uncertainty of whether AI may impact some established software and internet businesses:

In Australia, valuation multiples have come back in the past 6 months:

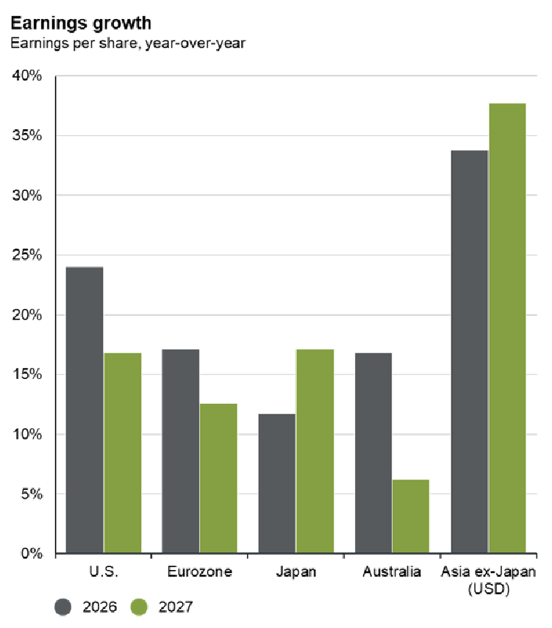

High valuations do not necessarily mean markets are about to fall. Valuations can remain above historical levels when profits are growing. Projected earnings in most markets remain buoyant, as this graph shows:

What this means for you

As always, there remains plenty of uncertainty for investors.

Global economic growth continues, corporate earnings remain positive and investment in technology is providing an important source of demand. Against that, inflation remains elevated, interest rates are restrictive and geopolitical risks have not disappeared.

This is not an environment that rewards confident short-term predictions.

It does reinforce the value of:

holding a diversified portfolio across asset classes, securities, companies, industries and countries;

avoiding excessive exposure to whichever investment theme is currently most popular;

maintaining sufficient defensive assets to meet your medium -term spending requirements;

rebalancing when market movements cause portfolios to meaningfully drift from their intended allocation; and

remaining invested through periods of uncertainty.

Investors are often tempted to wait until the outlook becomes clearer. Unfortunately, markets generally rise before the news feels comfortable.

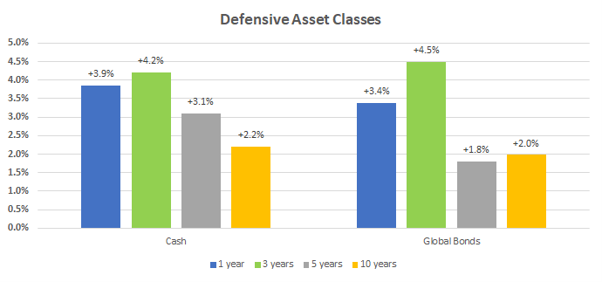

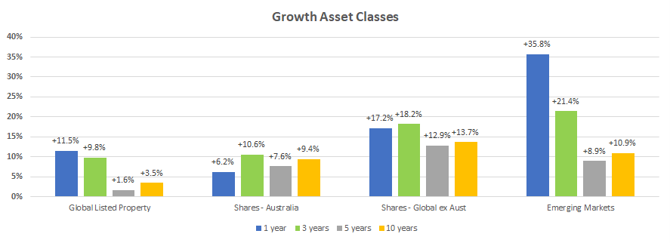

Returns of Major Asset Classes for Periods to 30 June 2026

Data sources:

Cash- Bloomberg AusBond Bank Bill Index

Global Bonds – Bloomberg Global Aggregate Bond Index 1-5 years

Global Listed Property – S&P Global Property Index (net div)

Shares Australia – ASX 300 Index (total return)

Shares – Global ex Australia – MSCI All Country World ex Aust Index (net div)

Emerging Markets – MSCI Emerging Markets Index (net div)